WetEV said:

GRA said:

It doesn't matter how rare it is, if someone decides they want that flexibility and are willing to pay for it.

But if most don't want it, and are not willing to pay for it.... Which we see by what EVSEs they buy. Why do you want to force everyone to get higher power OBCs?

In an ideal world I'd agree with you; I much prefer un-bundled options so I can pick and choose exactly what I want. We know things don't work that way. And I expect the extra cost of a 40 or 48A OBC vice a 32A is minimal, at least at mass-scale. BTW, here's an example of a new Mach-E owner trying to decide between a 40A EVSE with a plug versus a 48A hardwired one (essentially the same decision I'd have to make if given a free choice), with a variety of views expressed (including one the same as yours):

https://www.macheforum.com/site/threads/evse-48a-hardwired-vs-40a-plug-in.4416/ I guess we'll see what EVSE he buys, but it almost certainly won't be 32A.

WetEV said:

GRA said:

WetEV said:

Again, there is a rare case. L2 is cheaper to install than DCFC, and some remote places have higher power L2. Shorten your stay with a higher power OBC.

Which is the point. My ...

Again, pushing the rare case, trying to increase the cost and requirements of EVs. Spreading FUD with glee.

How is noting that all the cars the Ariya will be competing with come with 48A chargers, FUD? It's a fact.

WetEV said:

GRA said:

WetEV said:

Gain in usefulness per dollar spent, especially over the term of the car's production.

Yet they will clearly be competing with the ID.4, and assuming the price comes in a similar range the Ionic 5/EV6.

Competing by producing a slightly lower priced vehicle that does most of the same.

Outside of fleet sales, cars of close to comparable price are bought for specific features and personal preference, not a few hundred here or there. We still don't have a price for the Ariya, do we? But unless Nissan has cheaped out on everything, it's going to cost the same or considerably more than the ID.4 et al, because you're paying for an extra 8 kWh of battery - at say $150/kWh at the pack level (twice that retail), you're talking an extra $1,200 to produce it ($2,400 retail).

WetEV said:

GRA said:

WetEV said:

Total vehicle sales were down, but EV sales were almost flat.

As higher-pried cars took over the market.

EVs are now premium cars. As Rolls Royce recently figured out... in 1900.

https://www.caranddriver.com/news/a37770400/rolls-royce-spectre-ev-revealed/

Charles Rolls in 1900 said:

The electric car is perfectly noiseless and clean. There is no smell or vibration, and they should become very useful when fixed charging stations can be arranged.

While no price is announced, if you need to ask, you are not in the market for one.

Yet this changes, as the lowering cost of batteries is pushing the market for BEVs into lower prices. You too can buy a quieter, cleaner and smoother car... it is called a LEAF.

Sure, and have the battery die in a few years as I drive it repeatedly on steep climbs in the mountains and in hot desert areas. But since it simply lacks the range and charging speed I need, it's price is irrelevant to me.

WetEV said:

GRA said:

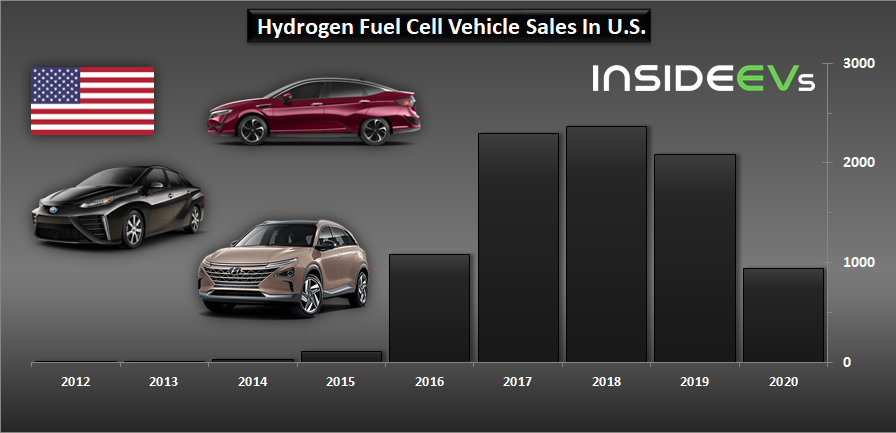

And we know why, lack of fuel in the 2nd half of 2019 stalled new station infrastructure, which carried on through 2020 due to Covid, plus lack of model choice.

You missed a key point. There is nothing what so ever that a driver cares about, that a hydrogen fuel cell car does better than a BEV.

Range? Drive across the USA in a BEV and see how far the hydrogen car goes.

Cost? Hydrogen will always be more expensive than electric power.

Pollution? Hydrogen is dirtier than coal... and likely to stay that way for decades.

Sure, could boost fool cell sales with more subsidies. A lot of BEVs are now sold with no or minimal subsidy.

Actually, there are several things a fuel cell does better than a BEV, and does them comparable to an ICE, which drivers overwhelmingly prefer to BEVs now, despite gas being generally more expensive (Of course, I'm a supporter of PHFCEVs for most people, to maximize the advantages and minimize the disadvantages of both techs). Better range, especially in winter, faster refueling to 100% (not just 80%), the ability to routinely use virtually all of the car's range with no degradation, longer life, just as clean if H2 is produced renewably. I note you once again ignore that California's retail H2 stations are using 90+% renewable H2 which has to meet the states' LCFS. Lack of ability to drive across the country is due to lack of infrastructure, just as BEVs were limited before their charging infrastructure was built, or fossil-fueled ICEs FTM. Until the station at Harris Ranch opened, you couldn't drive a Mirai between LA and SF or SAC; then you could.

BEV sales no less than FCEV sales remain dependent on subsidies, although the Bolt (once you can buy one again) is getting there. Speaking of FCEV sales in California, from the current Annual Evaluation:

Based on Department of Motor Vehicles (DMV) records of active FCEV registrations, California

had 7,993 on-road FCEVs as of April 1, 202112. Similar to reporting in prior years, the latest industry

estimates indicate a larger number of cumulative FCEV sales, at 10,665 in the United States by June

1, 2021 [13]. The COVID-19 pandemic significantly decreased sales across the automotive industry in

2020. Based on industry estimates, 2020 FCEV sales dropped more than 50 percent from any of the

prior three years of sales and were the lowest since 2015 [13]. Hydrogen supply constraints in 2020

and 2021 may have also played a role in reducing vehicle sales.

Although sales were markedly lower in 2020 due to the ongoing COVID-19 pandemic, the industry

appears to be on a path to recovery in 2021. Through June 1, 2021, industry estimates report 1,734

FCEV sales [13]. The FCEV sales volume to date in 2021 is already equal to 185 percent of the sales

in all of 2020 and 83 percent of the sales in all of 2019. The first quarter of 2021 was also the best-

selling quarter since industry tracking began in 2012 [13]. Stronger sales in 2021 are likely influenced

by the release of the redesigned 2021 model year Toyota Mirai.

The CEC’s December 2020 approval of awards in GFO-19-602 significantly strengthened the outlook

for hydrogen fueling infrastructure in California and could encourage a more aggressive auto

manufacturer outlook for future FCEV sales. Based on the most recent survey of auto manufacturers,

the industry appears to have regained confidence in sales potential through 2027. Updated

estimates project 30,800 FCEVs on the road as early as 2024 and 61,100 as early as 2027 as shown

in Figure ES 6. The near-term pace of deployment (through 2025) is similar to estimates based on

the 2020 survey, while projections for 2025 through 2027 have accelerated. In the past, long-term

projections (mostly in the Optional Period) have been higher than actual FCEV deployment while

near-term projections have been more accurate. . . .

12 The CEC’s ZEV Dashboard reports 7,129 FCEVs on the road at the end of 2020 [16]

https://ww2.arb.ca.gov/sites/default/files/2021-09/2021_AB-8_FINAL.pdf, page xix.

This is all a pointlessly repetitive argument, so I'll end this by putting down my marker. I say that if Nissan doesn't offer a higher than 32A OBC in the Ariya initially, it will do so no later than the car's MLU, quite possibly sooner. Whether it's included across the board or only offered on higher trims (as e.g. the RAV4Prime's faster OBC is, or the LEAF's once upon a time, not sure currently as I don't pay attention to LEAF trims anymore) I won't guess.

I take it you think they won't. As with your prediction that U.S. BEV sales (or was it PEV? I'll have to look it up) would reach 4% total this year, we'll see. The EPA's only guesstimating 8% by 2026; not sure if that's assuming the increased subsidies are passed, or not.